Over the past century, markets have crashed A DOZEN TIMES, several times by more than fifty percent, leaving people’s finances and dreams in disarray for YEARS. Not only is money lost, but TIME is lost. It takes time to build up a nest egg. The last thing anyone wants to do is to start over in retirement.

If you’ve been saving for thirty years for your dream retirement, it makes no sense to go back to where you were ten or fifteen years ago with your capital. Can it happen? Well, of course it DID happen—twice–in the last twenty years. The S & P is soaring like an eagle right now, but it got shot down like a duck in 2000 and 2008. Our parents taught us the slogan that “what goes up must come down.” They were right. But our parents couldn’t tell us the day or the hour. That’s why we plan.

We also learned in Boy Scouts to “Be Prepared.”

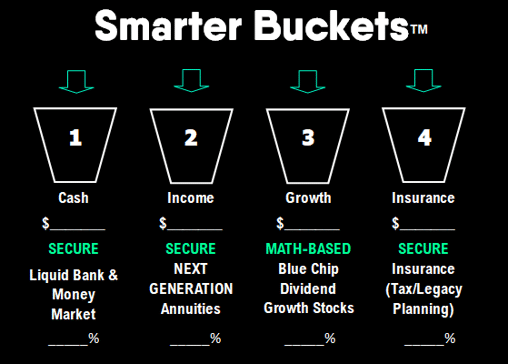

All of us have experienced investment losses after periods of euphoric gains. The best airplane in the world with the biggest gas tank still runs out of fuel one day. With the stock market, we know it’s not a matter of IF, but simply WHEN we see a correction. It’s part of life. But it shouldn’t impact your life. Your permanent money for income, preservation, and liquidity should be kept separate and apart from your risk capital. We call it bucket planning.

Bucket planning helps to put a firewall between the stock market and your

income capital. You already know how important it is to change your

investment focus as you retire. Your

time horizon shrinks and your risk

tolerance begins to disappear. That’s called having a case of the “normals.” It is simply wise stewardship to move from a

focus on pure accumulation to focusing on preservation and income . Sure, we

may want to grow our capital in retirement with prudent stock market

investments. But we need to avoid remaining saddled with perpetual risk

throughout our portfolio. Let’s only take risks that we need to take or want to

take.

Moderate risk with a portion of your money is a good idea, but it must be

kept in a separate bucket, away from your income capital. I call it Smarter

Bucketing. In planning for a worry-free

retirement, income replacement is job number one. Many people focus on

fees, rate of return, and taxes above all else. Those are all important

considerations in a well laid out plan. No one can argue that.

But the inarguable fact is that without reliable, secure cash flow, you don’t have a secure retirement. In order to be “set for life”, a smart goal, you will need more money coming in than going out from now on no matter what. Cash flow is king in retirement. Rather than trying to lasso and beat the market every week, being financially comfortable should be your primary goal.

With true financial security in first place on your list, planning becomes easier. You can first focus on having all the CASH FLOW to pay all bills and live in the lifestyle you choose–from now on. Then you allocate to liquidity. How much of your money do you want liquid at all times? Answering that question is key to beginning your overall allocation strategy.

Another phrase we have all grown up on is “Know Thyself.” This is your life and your personal situation. Don’t follow rules made for the “average” person. There is no average person, and you certainly don’t want to try to be one with your money. Your liquidity bucket is very important. Here is a practical way to approach allocating to liquid cash equivalents like money market accounts:

- Determine how much money you spend on a monthly basis and add twenty percent.

- It is wise to keep three to nine times that much in pure liquid money market and bank assets.

You are then prepared for emergencies, making you ready to take advantage of things like travel bargains, paying off credit cards, and feeling more confident about your financial plan. Here is a bit more parental advice: Don’t wear someone else’s shoes—wear your own.

After you have all the secure income and liquidity in place from reliable sources, you can then determine how much of your money should be kept at risk in the markets. Some people don’t want any risk in the markets, and that’s certainly fine if you have ample income, no debt, and have a cash flow plan to counteract inflation ten, twenty, and thirty years from now. Let’s not run out of money one day. Plan on the market being rough at times and for a year at a time. Markets recover but they can take their time doing it. Your stock investments are not about this month or this year. They are all about ten years from now and longer. Time rewards patient investors with sound strategies.

There are many approaches to the market. You can invest for growth only, or invest for dividends plus growth. Dividend investing takes time but the rewards can be more certain and longer lasting. How do you feel about the future of the stock market? Do you shoot for the moon with growth-only stocks, or do you start a dividend growth strategy, where you are constantly paid increasing dividends?

Growth-only portfolios are more risky. Dividend portfolios carry less risk and are the only form of stock portfolios where you are always getting a return—in the form of the dividend. You get that dividend even if the market goes flat, even if the market falls.

Even if you share prices temporarily dip, your dividends are not affected if you own the right blue chip companies. Solid companies keep paying those dividends (and many CEO’s jobs depend on) INCREASING the company’s dividend every single year without fail. The stock issued by those companies are known as Dividend GROWTH stocks, because you not only get paid every year to own your stocks, you get a RAISE every year!

If you are familiar with the story of the tortoise and the hare, as most of us are, you can think of a dividend growth portfolio as being your “tortoise strategy” and your growth and technology portfolio as the “hare” strategy. The right technology stocks should show steady growth into the decade ahead and will jump out at a faster pace, but we all should expect a few pull-backs along the way when the “rabbit needs a rest.”

Meanwhile your dividend growth portfolio will keep moseying along not getting tired, and paying you annually increasing dividends. And, if you are smart you will be reinvesting those dividends for several years before you tap into them for income. No matter which strategy you prefer, your stocks and ETFs belong in Bucket 3—separate and apart from your income and liquidity portfolio.

Eventually, with a dividend growth portfolio, you experience what is known as geometric compounding. In the days of higher interest rates, we used to say that you made interest on your principal and interest on your interest. That is exactly what happens with a dividend growth portfolio—made even better when held in an IRA or Roth IRA account and you reinvest dividends. A) Your dividends make you money, B) they buy you more shares every year, and C), those shares in turn pay increasing dividends, also buying new shares.

Eventually, you end up with a much higher yield on your original cost of getting into the dividend portfolio. What starts at a three or four percent dividend yield grows to five percent, then seven percent, and then ten percent over time through sheer mathematics, regardless of market fluctuations. Warren Buffett’s yield on his original investment in Coca Cola is now over fifty five percent, because of dividend increases and stock splits over time. All he did was let it work.

The IQ Wealth Black Diamond and Blue Diamond Dividend Growth Portfolios give an investor a prudent combination of dividends and technology for your growth bucket.

Growing your money is a fine goal, but without reliable recurring “forever”

income (like a pension), your retirement plan is still up in the air. That’s

why your income bucket is the key to your retirement.

In your income bucket, we help you select the nation’s finest uncapped principal secure index annuities with Guaranteed Lifetime Withdrawal Benefits that can pay you a lifetime secure income of from five to nine percent depending on age and deferral period.

Annuities are built for retirement. In retirement, risk-taking moves to the back seat. You want preservation and income sitting up front with you. The last thing you want is to go backwards. A market crash not only loses you money, it takes you back to where you were financially ten or fifteen years ago. No one wants that.

That’s where uncapped Next Generation retirement

annuities shine. There are zero management fees, and never a market loss. Ever.

If you are a day trader or always on the lookout for the next hot investment,

annuities are not for you.

If, however, you want to solidify your retirement, simplify your life, and

guarantee yourself a way to receive a steady and competitive income for life,

annuities should be considered. The annuities of old are a thing of the past.

You are wise to learn about, understand, and explore the newer, more flexible versions of

Next Generation retirement annuities.

Final word: Always consider the PURPOSE of your money when choosing any

investment. It isn’t a matter of whether stocks, ETFs, or annuities are

“better.” Each has it’s own special

capability and can be better than the other depending on what you are trying to

achieve. Are you looking mainly for safety, yield, and liquidity? A wise combination

of dividend and technology stocks, alongside safe secure annuities can provide

that. The IQ Wealth Smarter Bucketing system builds on a mathematically

allocated reasonable combination of all three. Let’s build a smarter bucket

strategy for you. Today, not tomorrow. Together, not alone.

Steve Jurich (pronounced Jur-itch) is a seasoned financial planner in Scottsdale, Arizona with clients in multiple states. He is a Kiplinger® Wealth Creation Contributor, an Accredited Invested Fiduciary®, and a Certified Annuity Specialist®